Introduction

“And oftentimes, to win us to our harm, The instruments of darkness tell us truths, Win us with honest trifles, to betray us In deepest consequence.”

— Macbeth, Act I, Scene III — Banquo to Macbeth, on the prophecies of the three Weird Sisters

PROLOGUE: THE THANE’S FATAL COMFORT

Shakespeare’s Macbeth is, among many other things, the most penetrating study in literature of the psychology of false security. The Thane of Glamis, Cawdor, and ultimately King of Scotland does not fall because he is foolish. He falls because he is too clever by half — because he takes the prophecies of the three Weird Sisters at face value, reads them as guarantees, and allows that comfort to erode the vigilance that is the only true guarantee a mortal can possess. When the witches tell him he ‘shall never vanquished be until Great Birnam Wood to high Dunsinane Hill shall come against him,’ Macbeth does not ask what manner of moving wood might be contrived. He hears what he wants to hear: that he is safe. The forest cannot move. Therefore, he cannot fall.

The forest moved. The branches were cut and carried by Malcolm’s advancing army. And Macbeth fell — not undone by the prophecy being false, but by it being misleadingly true. The witches told him no lie. They merely told him a truth so partial that it functioned as a perfect deception.

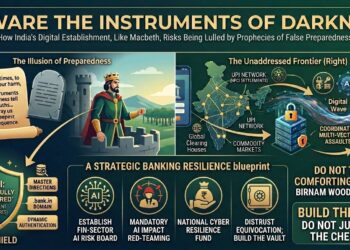

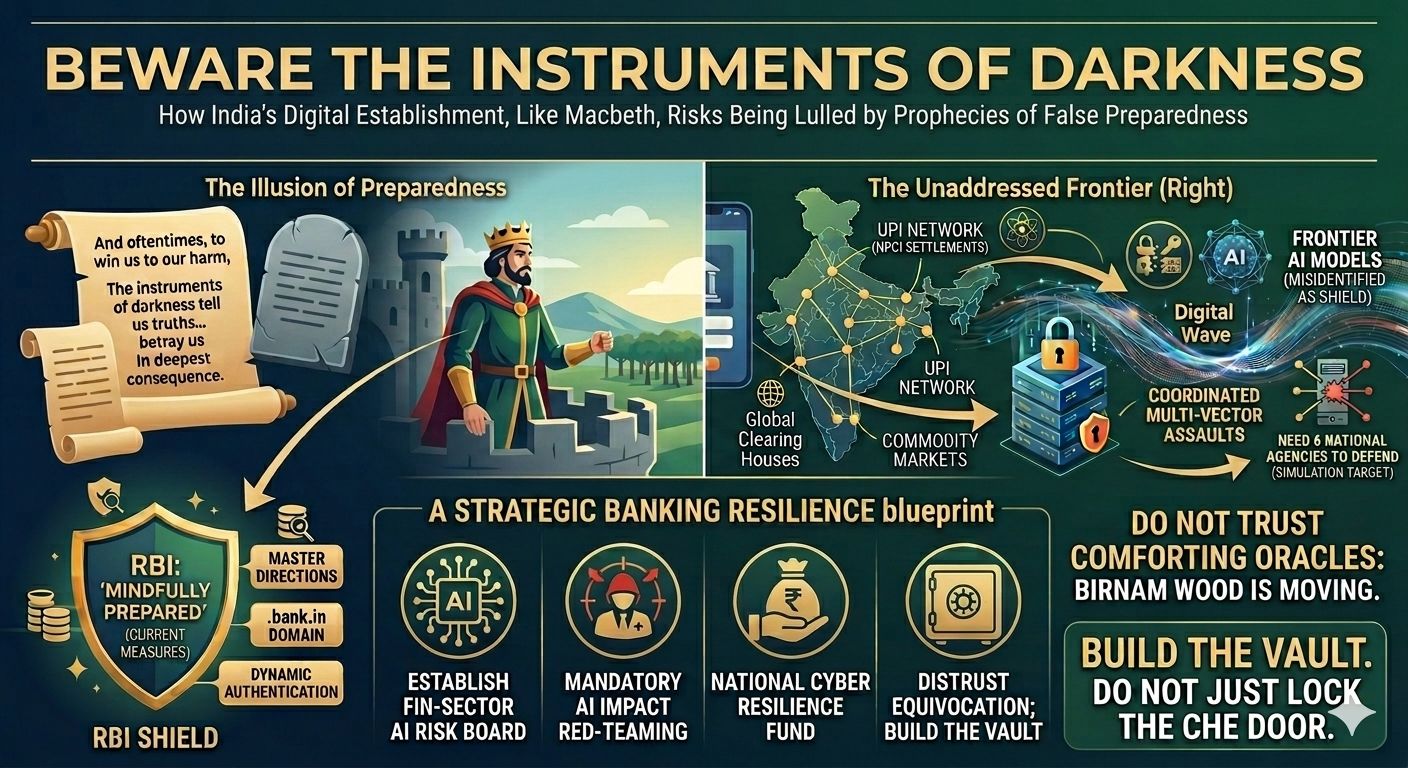

India’s digital establishment — its banking regulators, its senior bureaucrats, its financial sector sages — has, in recent weeks, issued its own prophecy of reassurance. Confronted with the emergence of Anthropic’s frontier AI model Claude Mythos Preview and its potential penetration into India’s financial ecosystem, the Reserve Bank of India’s Deputy Governor, Swaminathan J, stepped to the podium at the post-Monetary Policy Committee press conference on 6 June 2026 and delivered the institutional equivalent of Macbeth’s comfort: we are ‘mindfully prepared.’ Advisories have been issued. Systems are being monitored. The banking system is ready.

“We are mindfully prepared in terms of handling cyber security threats of this nature as well as the conventional nature.” — RBI Deputy Governor Swaminathan J, 6 June 2026.

Macbeth, too, was prepared for every army except one that moved.

This article argues that the Deputy Governor and his distinguished colleagues speak in entirely good faith. They are not witches. They are serious, experienced, and well-intentioned public servants doing their professional best. But good faith and adequate preparation are not synonyms — and the danger of the current moment is precisely that the language of preparedness, sincerely deployed, may be producing a false sense of security in the very institutions that can least afford it. The Birnam Wood of AI-enabled cyber warfare is already on the move. India needs to see it for what it is.

The Mythos Misidentification: When the Prophecy Itself Is Wrong

When RBI Deputy Governor Swaminathan J spoke of ‘Mythos-related cyber threats’ at the 6 June press conference, his concern was legitimate, and his instincts sound. But the framing reproduced uniformly across India’s financial press — from the Economic Times, Government to Business Standard to Hans India — rested on a foundational factual error, one that matters enormously for how the regulatory response is calibrated.

Claude Mythos Preview has been described in these reports as ‘an artificial intelligence-based cybersecurity system developed by Anthropic to detect software vulnerabilities and emerging cyber risks before malicious actors can exploit them.’ This is incorrect in every material particular. Mythos is not a cybersecurity platform. It is Anthropic’s most advanced frontier large language model — a general-purpose AI system of exceptional and deliberately restricted capability, withheld from public release not because it detects threats, but because it is itself a potential threat instrument of the first order. Access is limited to a small number of trusted organisations under Anthropic’s Project Glasswing, a programme whose precise contours Anthropic has not made public.

Here, the Macbeth parallel deepens. The Weird Sisters did not tell Macbeth false prophecies — they told him truths so selectively framed as to function as deceptions. The Indian financial press, and apparently the RBI’s briefing materials, have done something structurally similar: taken a real development (the emergence of a uniquely powerful AI system with potential Indian financial sector deployment), filtered it through a reassuring narrative (it is a cybersecurity tool, therefore it protects us), and produced a comfortable misreading that obscures the actual risk architecture.

Mythos is not a shield against cyber threats. It is a capability so powerful that Anthropic itself fears its misuse — which is why it has not been released to the public. This is what India’s banking regulators are actually managing.

The policy consequences of this misidentification are direct and serious. An institution that believes it is managing the integration of a defensive tool will adopt one set of risk controls — vendor due diligence, access protocols, and output monitoring. An institution that correctly understands it may be admitting into the financial system one of the most powerful AI systems ever built must adopt an entirely different governance architecture — adversarial red-teaming, autonomous decision-making constraints, hard limits on model access to transaction systems, and independent technical audit of model deployment. These are not minor procedural variations. They represent the difference between locking a door and building a vault.

The RBI’s own language reveals the analytical confusion. Deputy Governor Swaminathan spoke of ‘threats’ posed by Mythos in the same breath as describing ‘select corporates and financial entities’ having access to the project, as if the access itself were the threat vector. That intuition may in fact be exactly right. But it has not been articulated as a coherent risk framework. It is a correct instinct dressed in the wrong analysis, issuing reassurances based on the wrong diagnosis. This is the institutional Macbeth moment: the right general awareness of danger, paired with the wrong specific model of where the danger lies.

Credit and Critique: What the RBI Has Built, and What It Has Not

What Has Been Built

Justice requires acknowledging the genuine progress India’s financial regulators have made. The RBI’s 2024 Master Directions on IT Governance represent a substantive regulatory upgrade, mandating board-approved cybersecurity policies across all scheduled commercial banks, Security Operations Centres operating on a 24×7 basis, regular vulnerability assessments, and structured incident reporting with defined timelines. The Authentication Mechanisms for Digital Payment Transactions Directions of September 2025, which took effect on 1 April 2026, mark a real conceptual shift — moving from the brittle, SMS-OTP-based authentication regime to dynamic, risk-based verification that adapts to transaction context and behavioural signals. SIM-swap fraud cost victims nearly $50 million in 2023 alone; the new framework correctly identifies the telecom network as an unreliable security anchor and moves authentication to secured device hardware.

The mandate that all banking digital domains migrate exclusively to the .bank.in domain by October 2025 is architecturally sensible — restricting the domain space dramatically reduces the effectiveness of phishing and spoofed banking websites, cutting off one of the most common initial access pathways. UPI, which processes over 13.5 billion transactions monthly and accounts for approximately 80 per cent of all retail digital payments in India, is a genuine miracle of financial inclusion. The RBI has understood the scale of what it is protecting and has, within its existing conceptual framework, acted with reasonable diligence.

What Has Not Been Built — and Why That Is the Problem

But here is the Weird Sisters’ trick. Each of these measures is a genuine achievement — and each is, in the precise sense Banquo diagnosed, an ‘honest trifle.’ True enough to earn confidence. Insufficient to guarantee safety. The problem is not that the RBI has done nothing. The problem is that it has been calibrated to yesterday’s threat architecture, while the threat has moved — like Birnam Wood — into a category the existing framework was not designed to address.

The RBI has no dedicated AI risk taxonomy within its cybersecurity framework. AI-related threats are subsumed under ‘emerging technology risks’ — a category so broad as to be analytically useless when what is required is precise risk differentiation between, say, an LLM used for customer service chatbots, an AI model used for credit scoring, and a frontier system like Mythos deployed for financial analysis or regulatory interpretation. These are not the same risk profile. Treating them as such is like posting the same guard with the same instructions outside a post office and the nuclear command centre.

There is no mandatory pre-deployment AI impact assessment regime for systemically important financial institutions. There is no Financial Sector AI Risk Board — a body with the specific technical capability to evaluate frontier model architectures, as distinct from run-of-the-mill cybersecurity threats. And critically, inter-regulatory coordination between the RBI, SEBI, and IRDAI on AI risk remains advisory and ad hoc at a moment when the interconnections between banking, capital markets, and insurance create cascading failure pathways that no single regulator can map alone.

Deputy Governor Swaminathan’s assurance that the RBI ‘will keep the market informed once we have full details as to how we plan to handle this’ is, charitably read, appropriate epistemic humility. Less charitably, it is the sound of an institution that does not yet have a plan buying time while it formulates one. Macbeth, too, had plans. The problem was that his plans were based on the wrong intelligence.

The CBSE Attack: Birnam Wood Has Already Started Moving

On 2 June 2026, as lakhs of Class XII students sought to access the Central Board of Secondary Education’s post-result services portal for answer-sheet verification and rechecking, the portal came under what CBSE has described as a ‘coordinated’ cyber assault. The attack involved massive volumes of malicious internet traffic — preliminary assessments suggest an assault involving 3.8 million malicious packets — originating from multiple IP addresses within India and abroad. The attack pattern is consistent with a distributed denial-of-service operation designed to overwhelm the system, deny legitimate users access, and potentially probe for extraction vulnerabilities under the cover of the traffic storm.

CBSE has maintained that no data breach or unauthorised access was detected, and has filed a complaint with the Intelligence Fusion and Strategic Operations (IFSO) unit of Delhi Police. Repelling the attack required the simultaneous mobilisation of IIT Kanpur, IIT Madras, the Digital India Corporation, the Indian Cyber Crime Coordination Centre (I4C), and CERT-In. A formal Police complaint has been lodged. Six separate agencies of the national government were required to protect a school examination results portal.

It took the combined resources of six national agencies to defend a school results portal. What happens when the target is a clearing house, a stock exchange, or a bank’s core transaction engine?

This is not an argument that CBSE failed. The argument is that the level of institutional effort required to prevent failure reveals how thin the ordinary security margin is. If defending a portal handling student result verifications requires this scale of national mobilisation, the question that demands an answer is: what would a coordinated, high-sophistication attack on India’s UPI settlement infrastructure require? What would a simultaneous multi-vector assault on three mid-tier public sector banks look like? Has any institution in India’s financial system conducted a realistic simulation of that scenario — not a theoretical exercise, but a live drill with the kind of adversarial creativity that the CBSE attackers demonstrated?

The CBSE attack does not stand in isolation. India’s cyberspace has been identified as the second-most-targeted in the world. Between 2019 and 2023, cyber attacks on the Indian government increased by 138 per cent. In 2024, BSNL suffered a breach that exposed the data of millions of users — 278 gigabytes of data were stolen and offered for sale on the dark web. Multiple state e-governance portals were compromised in 2024, resulting in the leak of 2.5 million Aadhaar-linked citizen records. The 2022 AIIMS Delhi ransomware attack paralysed the hospital for weeks, potentially exposing the medical records of 4 crore patients. Indian educational institutions suffered more than 2 lakh cyberattacks and nearly 4 lakh data breaches over a nine-month study period from July 2023 to April 2024. BFSI sector attacks are rising at 25 per cent per annum, with potential annualised losses estimated at ₹50,000 crore.

Each of these incidents has been survived. Each has been followed by official assurances of lessons learned and systems strengthened. And each has been followed by the next attack, larger and more sophisticated than the last. This is the pattern that the instruments of darkness exploit: not the single decisive blow, but the incremental escalation against an adversary who mistakes survival for readiness.

The Structural Anatomy of India’s Cyber Exposure

The Legacy Infrastructure Trap

A significant proportion of India’s banking sector — particularly public sector banks, cooperative banks, and urban cooperative banks — operates on legacy core banking systems with insufficient encryption, inadequate patch management cycles, and structural failure to segregate front-end digital interfaces from back-end transaction engines. Replacing or upgrading this infrastructure requires capital investment and operational disruption that smaller institutions categorically lack the capacity to absorb. The RBI’s own compliance framework acknowledges this by imposing a lighter touch on NBFCs with assets below ₹500 crore — but the security of a networked system is determined by its weakest node, and India’s financial network has thousands of weakly secured nodes connected to its most critical arteries.

The Human Capital Deficit

Specialised cybersecurity expertise — particularly in AI security, offensive threat modelling, and zero-trust architecture design — remains acutely scarce in the Indian banking sector. Public sector institutions, bound by government pay scales and slow hiring processes, cannot compete for this talent against private banks, technology companies, and multinational firms. The result is that many banks’ Security Operations Centres are understaffed, under-trained, and dependent on third-party managed service providers whose own security postures are imperfectly monitored. The RBI rightly mandates third-party risk assessment — but mandating assessment is far easier than mandating genuine competence, and an audit report filed in a ring binder is not a security defence.

The Interconnectivity Cascade Risk

The same digital interconnectivity that makes India’s financial ecosystem so dynamically efficient has dramatically expanded its attack surface and created dangerous cascading failure pathways. RBI-regulated banks, SEBI-regulated stock exchanges and brokers, IRDAI-regulated insurance companies, and the NPCI-managed UPI infrastructure are interlinked in ways that no single regulator can fully map. A successful ransomware attack on a tier-two bank’s payment gateway does not stay within that bank. A DDoS attack timed to coincide with the opening of an auction for a major government securities issue could temporarily paralyse the primary market. A sophisticated intrusion into the core banking system of a large public-sector bank, if timed to coincide with settlement windows, could trigger cascading liquidity stress across the interbank market.

Inter-regulatory coordination among the RBI, SEBI, and IRDAI on cybersecurity risk remains ad hoc and advisory—a structure designed for normal times, not for the coordinated multi-vector attack that any serious state-level adversary would deploy in a crisis. Pakistan-affiliated hacktivists targeted Indian financial and government infrastructure during Operation Sindoor in May 2026. The BSE and NSE took the precautionary step of blocking their websites to international users. These were sensible defensive measures. They were also improvised, reactive, and driven by the specific geopolitical context — not by a pre-existing, exercised protocol.

The Digital India Paradox — Ambition Unmatched by Security Investment

This is the central, inescapable paradox of the Digital India programme: the ambition of the build has consistently and dramatically outrun the investment in security. Aadhaar, UPI, DigiLocker, the National Health Stack — these are genuine achievements of governance imagination and delivery, bringing hundreds of millions of Indians into the formal digital economy. But each new layer of digital public infrastructure added to the stack without proportionate security investment does not merely add its own risk — it multiplies the risk of everything beneath it, because each layer creates new attack surfaces, new credential databases, and new entry points into the entire ecosystem.

The CyberPeace Foundation’s Vineet Kumar captured this precisely: ‘Digitisation without cybersecurity is like building a house without doors or locks.’ The metaphor is apt. The Digital India programme has built extraordinary houses — and then, in too many cases, appointed a single elderly chowkidar with a lathi to guard the entire neighbourhood.

What Genuine Preparedness Requires: A Ten-Point Framework

The challenge is not primarily one of intent. Successive governments, the RBI, SEBI, and CERT-In have all demonstrated a sincere commitment to digital security. The challenge is of architectural coherence, institutional capacity, and the political will to invest in security at the same scale as connectivity. Macbeth was not short of intent either. He was short of accurate intelligence about the nature of the threat. The following framework attempts to provide that intelligence as an actionable prescription.

First: The RBI must constitute a dedicated Financial Sector AI Risk Board, entirely separate from its existing cybersecurity standing committee, staffed with technical experts capable of evaluating frontier model architectures. This body must develop India-specific risk taxonomies that distinguish between AI tools, AI systems, and frontier AI models, and prescribe differentiated governance requirements for each deployment category within regulated financial institutions.

Second: All systemically important financial institutions designated by the RBI must submit pre-deployment AI impact assessments before admitting any frontier model into operational systems. These assessments must include adversarial red-team exercises—not vendor-provided safety reports, but independent technical evaluations of what the model could do if its safeguards were circumvented or if it were accessed by a malicious insider.

Third: India requires a National Cyber Resilience Fund, modelled on the United Kingdom’s National Cyber Security Centre funding architecture, providing direct financial support to tier-two and tier-three banks, cooperative banks, and NBFCs that lack the capital to upgrade legacy infrastructure independently. The RBI cannot mandate security standards without ensuring that institutions have the resources to meet them.

Fourth: The inter-regulatory forum between the RBI, SEBI, and IRDAI must be upgraded from an advisory body to an operational Crisis Coordination Committee with real-time threat-sharing obligations, pre-agreed joint incident response protocols, and the authority to coordinate market-wide responses to systemic cyber events. The protocol must be exercised — drilled, tested, and refined — before the crisis that will require it arrives.

Fifth: CERT-In’s mandate and resources must be significantly expanded. The designation of Critical Information Infrastructure must be explicitly extended to cover the UPI settlement system, stock exchange matching engines, insurance data repositories, and — as the CBSE attack has demonstrated with brutal clarity — examination and credential systems. A DDoS attack on a school’s results portal during the critical post-result window is not an educational disruption; it is an assault on public trust in digital governance, and it must be treated with the same urgency as an attack on a bank.

Sixth: All central and state government digital service portals must be brought under a mandatory Government Digital Infrastructure Security Standard that specifies minimum requirements for DDoS mitigation capacity, encryption standards, penetration testing frequency, and incident response protocols. The standard must carry enforceable sanctions — not merely reporting obligations that fill the appendices of Annual Reports that no senior official reads.

Seventh: The Digital Personal Data Protection Act, 2023, must be implemented without further delay. The absence of a functioning Data Protection Board more than two years after the Act’s passage represents a regulatory failure of the first order. Without enforceable data protection accountability, there is no meaningful consequence for breaches — and without consequence, there is no institutional incentive for the behaviour change that genuine security requires.

Eighth: India must develop indigenous cybersecurity technology capacity through public research investment, procurement preferences for Indian-developed security tools, and sustained partnership between DRDO, IITs, and the private sector in AI-powered threat detection, post-quantum cryptography, and supply chain security auditing. Strategic dependence on foreign security technology for critical financial and public digital infrastructure is a vulnerability that no regulatory framework can fully compensate for.

Ninth: A mandatory National Cyber Stress Test — modelled on the RBI’s financial sector stress tests — must be instituted annually for all critical digital infrastructure, including stock exchanges, payment settlement systems, banking networks, and major government service portals. The test must simulate multi-vector, AI-enabled attacks — not the theoretical scenarios of yesterday’s threat model, but adversarial creativity calibrated to the capabilities that frontier AI models make available to a well-resourced attacker.

Tenth: India must engage seriously and urgently in the emerging international governance architecture for frontier AI in financial services — through the Financial Stability Board, the G20 Digital Economy Working Group, and bilateral arrangements with the United States, the European Union, and Singapore. Regulatory isolation in this domain is not sovereignty. It is exposure. The weapons that India’s adversaries may use against its financial system are being developed globally; the defences must be developed globally too.

Conclusion: Do Not Trust the Weird Sisters

Shakespeare gives Macbeth one moment of clear sight. In Act V, when the messenger brings him the news that Birnam Wood is indeed moving toward Dunsinane, the scales briefly fall. ‘I pull in resolution,’ he says, ‘and begin to doubt the equivocation of the fiend that lies like truth.’ He knows, in that instant, that he has been deceived — not by a lie, but by a truth so partial as to function as a lie. He knows it a moment too late.

India’s digital establishment has time. The forest is moving, but it has not yet reached Dunsinane. The RBI’s senior leadership — distinguished public servants of proven competence and genuine good faith — are not the villains of this piece. Deputy Governor Swaminathan J’s assurances are not cynical; they reflect the genuine conviction of an institution that has worked seriously at a hard problem. The danger is not bad faith. The danger is the specific, well-documented human tendency to mistake yesterday’s preparations for tomorrow’s readiness.

The CBSE attack on 2 June 2026 targeted not a bank, not a power grid, not a defence installation, but a school examination portal — and it required six national agencies to repel it. The Mythos episode has revealed that India’s financial regulators are managing a frontier AI deployment they do not yet fully understand, offering reassurances calibrated to a risk they have misdiagnosed. And the data shows that BFSI sector attacks are rising by 25 per cent per annum, that India is the second-most-targeted cyberspace in the world, and that each attack has been more sophisticated than the last.

The instruments of darkness tell us truths. They tell us we have issued advisories. They tell us our SOCs are operational. They tell us authentication has been upgraded. They tell us the banking system is resilient. And all of these things are, in their way, true. True enough to lull. Not enough to save.

India has built the world’s most ambitious digital public infrastructure. It must now build the security architecture to match — before the forest arrives at Dunsinane, and the equivocation of the fiend is laid bare.

The prescription is available. The expertise exists. The institutional will must be summoned. The RBI, the Government of India, SEBI, IRDAI, CERT-In, and the entire apparatus of the Digital India programme must confront, with clear eyes and without the comfort of reassuring prophecies, the nature of the threat that is already moving toward them.

Macbeth could have survived. He had the walls of Dunsinane, a trained army, and forewarning. What he lacked was the discipline to distrust a comforting oracle. India has the institutions, the talent, the technical capacity, and — critically — the time. What it must not lack is the discipline to distrust the comfortable prophecies of its own making.